Anti-dilution protection Fundraising

Anti-dilution protection mechanisms: Full ratchet or weighted average ratchet, what’s the difference?

1 April 2026

You have discerned that a ratchet protects investors when the company raises funds at a lower valuation than the valuation retained for their investment via anti-dilution subscription rights, giving them the right to subscribe – for a symbolic amount – to a certain number of shares in the event of a downround.

Ratchet mechanisms generally fall into two types:

- Full ratchet anti-dilution protection effectively fully lowers the subscription price of the original investment to the subscription price of the down round.

As a result, the investors benefiting from the ratchet receive a number of additional shares equal to the difference in shares issued based on the original subscription price and the subscription price of the down round.

As such, it is important to provide for a reasonable monetary threshold (a minimum investment amount) in order for a down round to trigger a full ratchet anti-dilution protection. Otherwise, even a very limited (bridge) down round would indirectly lead to an entirely disproportionate dilution. This is why a convertible loan is an often utilized tool by shareholders in such a context.

- Weighted average ratchet anti-dilution protection lowers the subscription price of the original investment to the average subscription price of the original investment and the subscription price of the down round taking into account the weight of the different investment rounds.

- Broad based weighted average ratchet anti-dilution protection is calculated by reference to the company’s fully diluted equity (i.e. including convertible securities such as warrants and stock-options).

- Narrow based weighted average ratchet anti-dilution protection is calculated by only taking into account the company’s issued shares (i.e. only the existing and the newly issued shares, excluding convertible securities).

A full ratchet will always result in a better protection for its beneficiaries than a weighted average ratchet and, therefore, is more detrimental to existing shareholders than a weighted average ratchet.

Given that a broad based weighted average ratchet will take into account more securities to set the reference value of the shares, it should result in a lower protection for the beneficiaries of the ratchet compared to the narrow based weighted average ratchet.

Our experience at Beyond tells us that, when the principle of a ratchet is accepted by the existing shareholders, the narrow based weighted average ratchet is the anti-dilution protection mechanism retained by most parties.

How does this translate in terms of numbers?

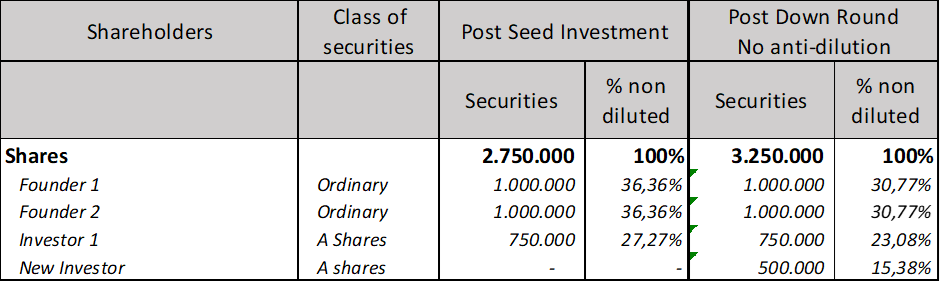

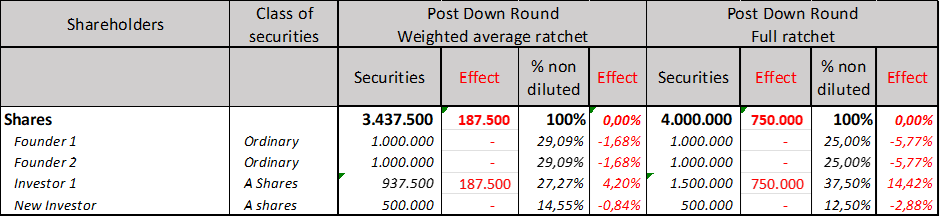

Below you will find an example visualizing the consequences of a down round (€ 250.000 invested at € 0,50 / share) occurring after a seed investment round (€ 750.000 invested at € 1 per share) with/without anti-dilution protection, including the difference between a full ratchet and a weighted ratchet approach.

As the cap table is modelled after a seed investment round, the founder’s shares are not taken into account for the calculations. Moreover, for the sake of simplicity, the example does not illustrate any difference between a narrow based weighted average ratchet or a broad based weighted average ratchet (the latter being rarely used based on our practice).

- Example without ratchet mechanism

- Example with ratchet mechanism

Want to see the impact of a ratchet on your shareholding? Visit our page dedicated to our simulators: you can apply these mechanisms to your cap table and compare different scenarios in just a few clicks.

Specializing in tech and digital, Beyond Law Firm assists innovative companies with their legal affairs.

Let's talk